Introduction: Why This Matters in 2025

If you sold your Arizona home tomorrow, do you know how much of that money you’d actually keep?

Many homeowners assume there’s no tax on the sale of a primary residence. The truth? It depends.

If you’ve lived in Arizona for a while, chances are your home has appreciated significantly. And while that’s good news, it also raises an important question: what happens when you sell?

The IRS has rules that can protect a portion of your gain — but only if you qualify. To know for sure, you need to understand your cost basis: what you paid for the property, plus documented improvements you made over the years.

And let me be clear upfront: this blog is for education only. Every seller’s situation is different. Always consult your CPA or qualified tax advisor before making financial decisions.

What Is Capital Gains Tax?

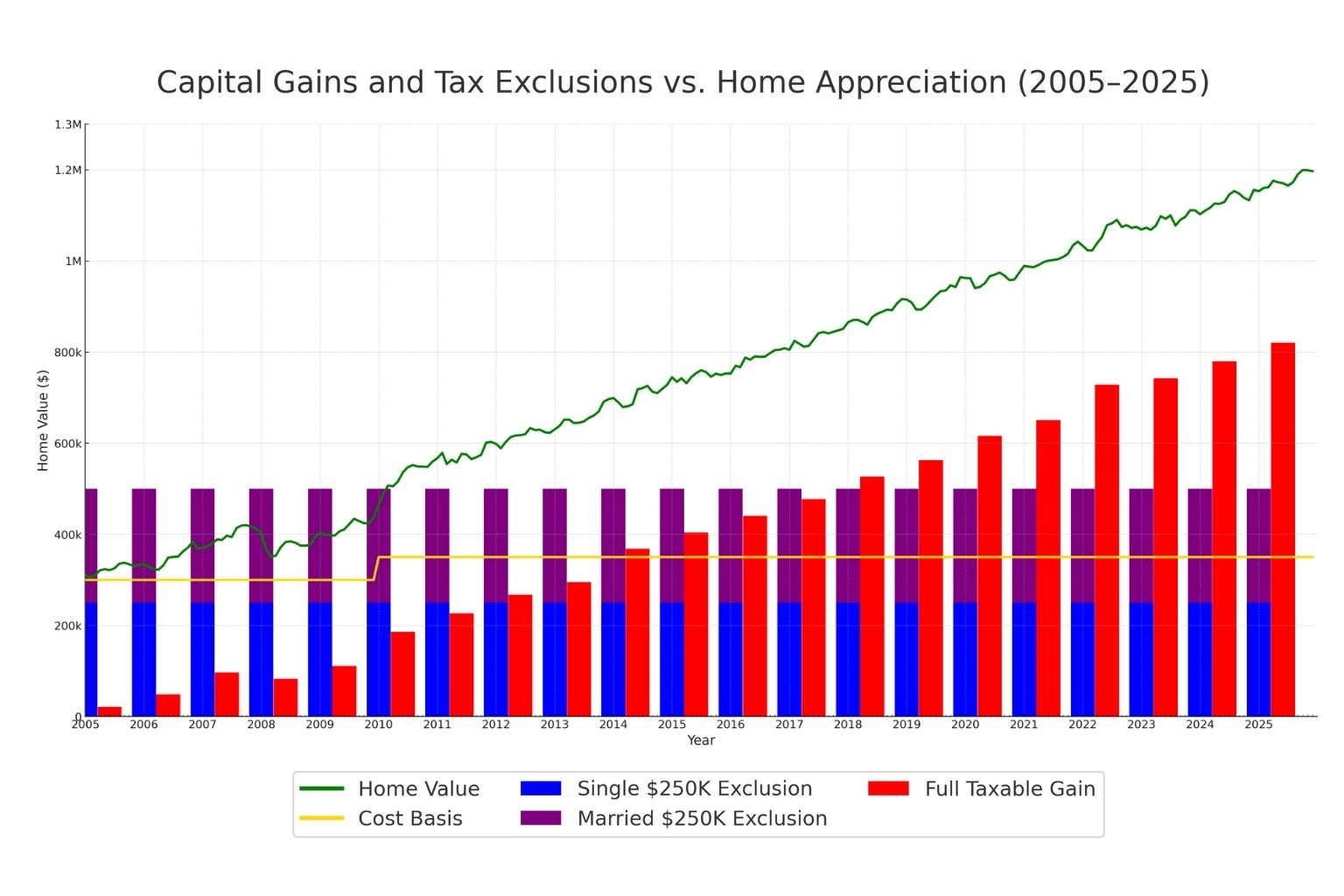

When you sell your home, the IRS looks at your gain — not your sales price.

Here’s the formula:

Sale Price – Adjusted Cost Basis – Selling Costs = Gain

- Sale price is what you sold the home for.

- Adjusted cost basis is what you originally paid, plus certain improvements, minus any depreciation (if you rented the property at some point).

- Selling costs include things like real estate commissions and closing fees.

👉 Example:

- You bought your Gilbert home in 2005 for $250,000.

- You spent $50,000 remodeling the kitchen and adding solar panels (with receipts).

- Your adjusted cost basis is now $300,000.

- In 2025, you sell the home for $800,000.

- Selling costs total $48,000.

Your gain = $800,000 – $48,000 – $300,000 = $452,000.

Does that mean you owe tax on $452,000? Not necessarily. That’s where the IRS exclusion comes in.

Home Improvements vs. Routine Maintenance: What Really Counts Toward Cost Basis

This is where many sellers get confused. Not all money you spend on your home increases your cost basis. The IRS draws a line between capital improvements and routine maintenance.

Capital Improvements (Increase Basis)

These add to your home’s value, extend its life, or adapt it for new use. Examples:

- Kitchen or bathroom remodel

- Adding a bedroom, deck, or garage

- Installing new HVAC, roof, or solar panels

- Upgrading electrical, plumbing, or windows

- Finishing a basement or adding square footage

- Certain landscaping projects, like replacing a driveway damaged by tree roots, or removing trees that were undermining the foundation

✅ These expenses usually increase your cost basis, reducing taxable gain when you sell.

Always confirm with your CPA which improvements qualify.

Routine Maintenance (Does NOT Increase Basis)

These are ordinary repairs that preserve your home but don’t add long-term value. Examples:

- Trimming trees or routine lawn care

- Fixing a faucet or toilet

- Replacing broken appliances

- Painting (unless part of a major remodel)

- Patching a roof leak

- Pest control

❌ These costs typically do not increase your basis.

When in doubt, check with your tax advisor.

Pro Tip:

“If the work makes your home better than it was before, it may count. If it just keeps your home the same, it usually doesn’t. Save receipts for the big-ticket projects — then let your CPA sort the gray areas. That one step could save you thousands in taxes when you sell.”

The Primary Residence Exclusion (IRS Section 121)

Here’s where the good news comes in. The IRS allows you to exclude a portion of your gain if the property was your primary residence.

- $250,000 tax-free for an individual seller

- $500,000 tax-free for a married couple filing jointly

To qualify, you must have:

- Owned and lived in the home for at least 2 of the last 5 years before the sale

- Not used the exclusion on another home sale in the last 2 years

This exclusion can be used once every two years.

Pro note:

“Think of this as one of the IRS’s few true tax-free gifts. But like every gift, it comes with conditions. Meet them, and you can keep up to half a million in profit, tax-free.”

👉 Reminder: rules can be nuanced — always confirm with your tax advisor how this applies to you.

Filing as a Couple

Married couples must file jointly to use the full $500,000 exclusion. If filing separately, each spouse can only claim up to $250,000. Even if only one spouse is on title, the couple may still qualify for the full $500,000 exclusion if they file jointly and both meet the residency requirement.

As always, check with your tax expert for your particular tax situation.

Adding Someone to the Deed: Proceed with Caution

Some parents add a child to the deed of their home, thinking it’s the easiest way to pass the property on. But this decision can create unexpected tax consequences:

- If the child hasn’t lived in the home as a primary residence, they won’t qualify for the Section 121 exclusion. When the home is sold, their share of the gain may be fully taxable.

- By being on the deed, the child may also miss out on a step-up in basis that would have applied if they inherited the home instead. That step-up often eliminates decades of gain, but it’s lost if the transfer happens during the parents’ lifetime.

- In some cases, it can also complicate financing, refinancing, or eligibility for certain estate planning strategies.

👉 Another good reason to consult with a tax and estate planning professional before changing title. What seems like a simple solution can create costly problems down the road.

Better Options for Passing on Your Home

Instead of adding a child directly to the deed, consider working with an estate planning attorney on alternatives such as:

- A Beneficiary Deed – In Arizona, this allows the home to transfer directly to your heirs upon death, avoiding probate.

- A Living Trust – The home is held in trust and passes to your beneficiaries under the trust’s terms, often with smoother administration and tax advantages.

Both of these approaches typically preserve the step-up in basis at inheritance, helping your children avoid unnecessary capital gains taxes.

Fail to Plan or Plan to Fail

Keeping a well-organized file on your home can save you both money and stress later. Homeowners should:

- Save receipts and records for all repairs and improvements. These documents support warranty claims and help establish your cost basis for tax purposes.

- Track service providers in case follow-up or warranty work is needed.

- Ask about warranties when work is completed—especially for big-ticket items like AC systems, roofs, or water heaters. Confirm whether those warranties are transferable to a new owner.

When you eventually sell, being able to provide a buyer with transferable warranties adds value and peace of mind, making your home more attractive.

Top Pitfalls Homeowners Should Avoid

Even well-intentioned sellers can get tripped up by details. A few of the most common mistakes include:

- Missing the 2-out-of-5 year rule

Waiting too long to sell—or moving out too early—can disqualify you from the exclusion. Note: the sale must be completed by the end of the 5th year, so if you plan to sell, make sure your home goes on the market early enough to close before the deadline. - Confusing maintenance with improvements

Replacing a faucet or trimming trees won’t raise your cost basis, but a new roof or HVAC system will. - Overlooking partial business or rental use

If part of your home was used for business or rented (for example, a home office you depreciated on taxes), that portion may not qualify for the exclusion, and any depreciation taken has to be “recaptured” and taxed. - Failing to file jointly when eligible

Married couples who don’t file jointly may leave $250,000 of exclusion on the table. - Poor recordkeeping

Not saving receipts, warranties, or contractor information can cost you thousands in missed deductions and buyer confidence.

👉 As always, consult with a qualified tax specialist about your particular situation. Every homeowner’s numbers and history are different.

Frequently Asked: Common Questions Sellers Ask

Whenever I bring up capital gains at a seminar or client meeting, these are the first questions that come up:

“Do I always avoid taxes when selling my primary home?”

Not always. It depends on whether your gain is under the $250,000 (single) or $500,000 (married filing jointly) exclusion, and whether you’ve met the 2-of-5 year residency test.

“How do I calculate my cost basis?”

Start with what you paid for the home. Add in documented improvements (receipts matter), and subtract depreciation if you ever rented it.

“Can we use the $500,000 exclusion if only one spouse owns the home?”

Yes — if you’re married and filing jointly, and both meet the use test while at least one meets the ownership test, you can still qualify for the full $500,000.

“What if part of the home was rented or used for business?”

The exclusion only applies to the portion used as a primary residence. The rental or business portion may still be taxable, and any depreciation must be recaptured.

“Can I use the exclusion more than once?”

Yes — but only once every two years.

“Do I have to report the sale if my entire gain is excluded?”

Yes, if you receive a Form 1099-S from the title company, you must report it, even if your gain is fully excluded.

👉 Important: These are general rules. Every tax situation is different. Always confirm your numbers with a CPA.

More Real-World FAQs — The Questions That Trip Folks Up

“Can I deduct a loss if I sell my home below what I paid?”

No. Losses on the sale of a personal residence are not deductible.

“What counts as an improvement versus a repair?”

Adding a new room, installing solar, or replacing a roof = improvement. Fixing a faucet, patching a leak, or trimming trees = maintenance. Improvements count toward basis; repairs don’t.

“How much tax do I pay if my gain is above the exclusion?”

Long-term capital gains are usually taxed at 0%, 15%, or 20% depending on your income. High-income sellers may also pay a 3.8% Net Investment Income Tax (NIIT).

“What if I don’t meet the full 2 years?”

Partial exclusions are sometimes available if you had to sell due to job relocation, health reasons, or unforeseen circumstances.

Again — these are areas where your CPA is your best resource.

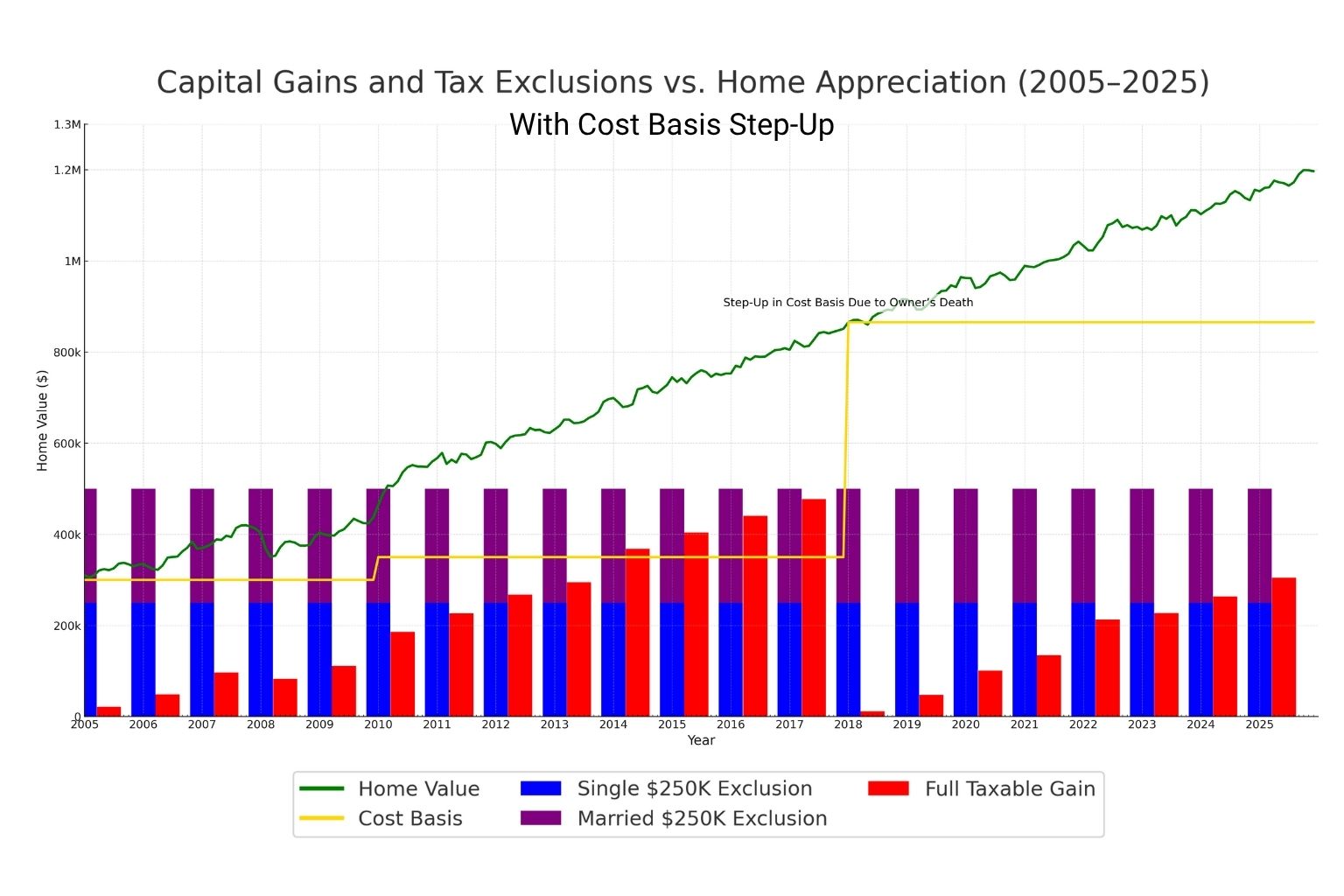

Special Case: What If One Spouse Dies?

This one is especially important, and often overlooked.

When one spouse passes away, the surviving spouse typically receives a step-up in cost basis on the deceased spouse’s share of the property. In most states, that means only half the property gets a step-up.

But Arizona is different. Because Arizona is a community property state, the surviving spouse receives a 100% step-up in basis for the entire home — not just 50%.

👉 Example:

- A couple bought their Phoenix home for $200,000 years ago.

- At the husband’s passing, the home is worth $800,000.

- In a non-community property state, the wife’s new basis would be $500,000 (her $100K original half + $400K stepped-up half). If she sold for $800,000, she’d show a $300,000 gain.

- In Arizona, her new basis is $800,000 — the full market value at the time of death. If she sold right away, she’d show no gain at all.

Even better, the surviving spouse can still claim the full $500,000 exclusion under Section 121 — as long as the home is sold within two years of the spouse’s death. After that, the exclusion drops back to $250,000.

Pro note:

“This is one of those windows of opportunity most families miss. In Arizona, the rules are even more favorable — but only if you know them. Don’t wait too long. Sit down with your CPA and create a plan before you list.”

Case Studies: How Planning Saves Sellers Thousands

Let’s make this real with a few Arizona examples:

📖 Case Study #1: The Scottsdale Couple Who Saved Six Figures

- Situation:

A couple in Scottsdale bought their home in 1998 for $250,000. By 2025, it was worth $1,000,000. - Their assumption:

“It’s our home, so we won’t pay any taxes when we sell.” - The reality:

Their cost basis was $250,000 + $50,000 in improvements. That left them with a $700,000 gain.

The IRS only excludes $500,000 (married filing jointly). The remaining $200,000 would be taxable. - The risk:

If they had gone straight to market without planning, they might not have gathered improvement receipts or confirmed their residency timeline. In that case, even if they saw their accountant afterward, the CPA’s hands would have been tied — they’d have to report the $700,000 gain, creating a six-figure tax bill. - What happened instead:

They met with us first. We asked the right questions, confirmed they qualified for the $500,000 exclusion, and looped in their CPA. Together, we reduced their taxable gain from $700,000 to $200,000 — saving them over $100,000 in taxes.

📖 Case Study #2: The Chandler Widow Who Sold at the Right Time

- Situation:

A couple in Chandler bought their home for $200,000. When the husband passed away in 2023, the home’s market value was $800,000. - Step-up in basis (Arizona’s advantage):

Because Arizona is a community property state, the wife received a 100% step-up in basis to $800,000 at her husband’s death. If she had sold immediately, there would have been no taxable gain. - What happened next:

She held onto the home for two more years, and by 2025 it was worth $1,000,000. - The risk:

If she had waited until 2026 (past the 2-year window), she would only have been entitled to the $250,000 exclusion as a single filer. Her gain would have been $200,000, leaving $50,000 taxable. - What she did instead:

She sold in 2025, still within the 2-year window. That allowed her to use the $500,000 exclusion available to surviving spouses. With her CPA’s guidance, her $200,000 gain was fully excluded. - Result:

By selling in time, she avoided a $10,000–$30,000 tax bill (depending on her tax bracket).

✅ Why This Works for Arizona

- The community property step-up eliminated her husband’s lifetime gain.

- The 2-year surviving spouse rule allowed her to shield post-death appreciation from tax, up to $500,000 instead of just $250,000.

- Together, they protected her equity and gave her flexibility in downsizing.

📖 Case Study #3: The Paradise Valley Family Who Paid the Price

- Situation:

A homeowner in Paradise Valley added his children to the title of his $1.2M home in 2022, thinking it would “help them” later. His cost basis was $300,000. - What went wrong:

By gifting the home during his lifetime, his children inherited his carry-over basis of $300,000. When they sold for $1.2M, the CPA had no choice but to report a $900,000 gain — creating a tax bill of nearly $180,000. - The missed opportunity:

If the father had kept the home in his name and passed it through inheritance, his children would have received a step-up in basis to $1.2M. They could have sold immediately with no capital gains tax due. - The takeaway:

His CPA could only work with the decision already made. Had the family asked the question earlier, they could have avoided the entire tax bill.

Real-Life Example: Arizona Home Sale in 2025

Let’s put it all together with a realistic scenario.

- A couple bought their Phoenix home in 2005 for $300,000.

- Over the years, they invested $50,000 in improvements — kitchen remodel, upgraded windows, and a new roof (with receipts).

- Their adjusted cost basis = $350,000.

- In 2025, they sell the home for $900,000.

- Selling costs (commissions, title, escrow, fees) = $60,000.

Gain calculation: $900,000 – $60,000 (selling costs) – $350,000 (basis) = $490,000 gain.

Exclusion (married filing jointly): $500,000.

Taxable gain: $0.

👉 Without documenting their improvements, their basis would have been only $300,000. In that case, their gain would have been:

$900,000 – $60,000 – $300,000 = $540,000 gain.

After the $500,000 exclusion, they’d pay tax on $40,000.

Lesson: Saving receipts for improvements turned a taxable gain into a tax-free sale.

Arizona Sellers’ 2025 Checklist

Before you list your home, gather:

- Original purchase documents

- Receipts for major improvements (kitchen, bath, roof, solar, HVAC, additions)

- Settlement statements from any refinance or purchase

- Appraisals, especially if you inherited the property (date-of-death appraisal)

✅ Step 1: Call your CPA with these documents.

✅ Step 2: Sit down with a planner (like me) to run the scenarios before you list.

Common Mistakes to Avoid

- Selling before meeting the 2-year residency rule.

- Assuming all primary home sales are automatically tax-free.

- Failing to keep receipts for improvements.

- Adding kids to the title too early (triggering carry-over basis instead of step-up).

- Forgetting the 2-year window after a spouse’s death.

- Failing to get a date-of-death appraisal. This is one of the most costly mistakes in Arizona. Without an appraisal, you may lose the ability to prove your stepped-up basis — leaving your CPA no choice but to report a higher gain than necessary.

Pro note:

“These aren’t just tax rules — they’re opportunities to protect your family’s wealth. Don’t miss them.”

Arizona-Specific Notes

- Capital gains and Arizona taxes: Arizona does not impose a separate state-level capital gains tax. Instead, gains flow through as part of your Arizona income tax. This is far less punishing than states like California (13.3% state capital gains), but it still impacts your return — especially in high-appreciation markets like Scottsdale, Paradise Valley, and parts of Phoenix.

- Community property and the step-up in basis: Arizona is a community property state, which means when one spouse passes away, the surviving spouse receives a 100% step-up in basis for the entire home — not just 50%. To take advantage of this, you must obtain a professional appraisal at the time of death. Without that, the IRS could challenge your stepped-up basis later.

Pro note:

“In Arizona, the rules are in your favor — but only if you do the paperwork. The step-up is one of the most powerful tools for protecting your family’s wealth, and it starts with an appraisal at the right time.”

Busting Common Myths

- ❌ “You never pay taxes on selling your home.”

✅ Truth: Only if your gain is under the exclusion and you meet the requirements. - ❌ “All repairs add to my cost basis.”

✅ Truth: Only capital improvements do. Routine maintenance doesn’t count. - ❌ “Adding my kids to the title helps them avoid taxes later.”

✅ Truth: It often does the opposite — they inherit your basis and your tax liability.

Pro tip:

“The IRS doesn’t care about what your neighbor said. They care about your paperwork.”

Next Steps: Planning Ahead, Even If You’re Not Selling Today

You may not be ready to sell this year, but the decisions you make now will shape your options later. Here’s how to stay prepared:

- Track improvements with receipts and photos to protect your cost basis.

- Know your timelines if you’re nearing the 2-out-of-5-year rule, or if life changes (retirement, downsizing, a spouse passing) may affect when you sell.

- Ask about warranties whenever you replace big-ticket items—transferable warranties can boost buyer confidence down the road.

- Build your team early by connecting with a Realtor, tax specialist, and financial advisor so you know who to call when the time comes.

Key Takeaways

- Section 121 exclusion lets you keep more of your home sale profits—up to $250K single or $500K married filing jointly.

- The death of a spouse may extend the higher exclusion for up to two years.

- Home improvements (not routine maintenance) increase your cost basis and reduce taxable gain.

- Filing jointly matters for couples, even if only one spouse is on title.

- Adding someone to the deed may create unintended tax consequences—explore better alternatives like a beneficiary deed or trust.

- Organized recordkeeping protects you, adds buyer value, and can reduce taxes.

- Every situation is unique—consult a tax accountant to confirm your numbers before you sell.

Considering a Sale? Don’t Let Taxes Take You by Surprise.

As part of the KW Real Estate Planner community, I help Arizona homeowners understand how the timing of a sale and their unique situation can affect capital gains taxes. While I don’t provide tax advice, I’ll walk you through your options, connect you with trusted professionals, and help you make the most of your equity.

📞 Call me at 602-770-0643 or email scoomer@kw.com to schedule your complimentary Capital Gains Planning Session and learn how to protect your hard-earned profits.