Why Understanding Your Mortgage Matters in Today’s Arizona Market

Buying a home in Arizona often starts with one big question: How will I finance it?

With interest rates shifting — and possible rate drops on the horizon — buyers who prepare now can move quickly when opportunities arise. This guide will walk you step-by-step through the mortgage process so you can secure the best loan for your situation.

What Is a Home Mortgage?

A home mortgage is a loan you take out to purchase residential property. For most Arizona buyers, it’s the gateway to homeownership. Whether you’re:

- A first-time buyer

- A move-up buyer

- Downsizing

…your mortgage choice impacts your monthly payment, total interest paid, and how quickly you build equity.

How to Qualify for a Mortgage in Arizona

1. Find the Right Lender

- Local mortgage broker or bank for personalized guidance.

- Online lender for convenience and faster approvals.

- Ask your real estate agent for trusted referrals.

2. Income & Employment History

- Most lenders require two years in the same job or field.

- Recent graduates may qualify with proof of future employment.

3. Credit Score Requirements

- Conventional loan: Typically 620+

- FHA loan: As low as 580

- VA loan: Flexible with strong income history

- Higher scores mean lower interest rates and better terms.

How Mortgage Payments Are Calculated

Your monthly payment usually includes:

- Principal – the portion reducing your loan balance.

- Interest – the lender’s charge for borrowing money.

- Property Taxes – collected by your lender and paid on your behalf.

- Homeowner’s Insurance – protects against fire, theft, or disasters.

- Private Mortgage Insurance (PMI) / Mortgage Insurance Premium (MIP) – depends on loan type and down payment.

FHA Loans & Mortgage Insurance: What Buyers Should Know

FHA loans are popular in Arizona for their flexible credit requirements and low down payment options, but they require mortgage insurance (MIP) on every loan, no matter how much you put down.

Here’s what that means:

- Upfront MIP: 1.75% of the loan amount, paid at closing (often rolled into the loan).

- Annual MIP: Paid monthly, based on your loan amount and term.

How Long You’ll Pay MIP:

- Less than 10% down: MIP is required for the life of the loan.

- 10% down or more (even 20%+): MIP is required for 11 years before it drops off.

This is different from conventional PMI, which can be removed once you reach 20% equity. With FHA, the only way to eliminate it earlier is to refinance into a conventional loan once you meet equity and credit requirements.

👉 Key takeaway: FHA is an excellent tool for getting into a home, but if you’re putting 20% down, compare it to a conventional loan — you may save on insurance costs in the long run.

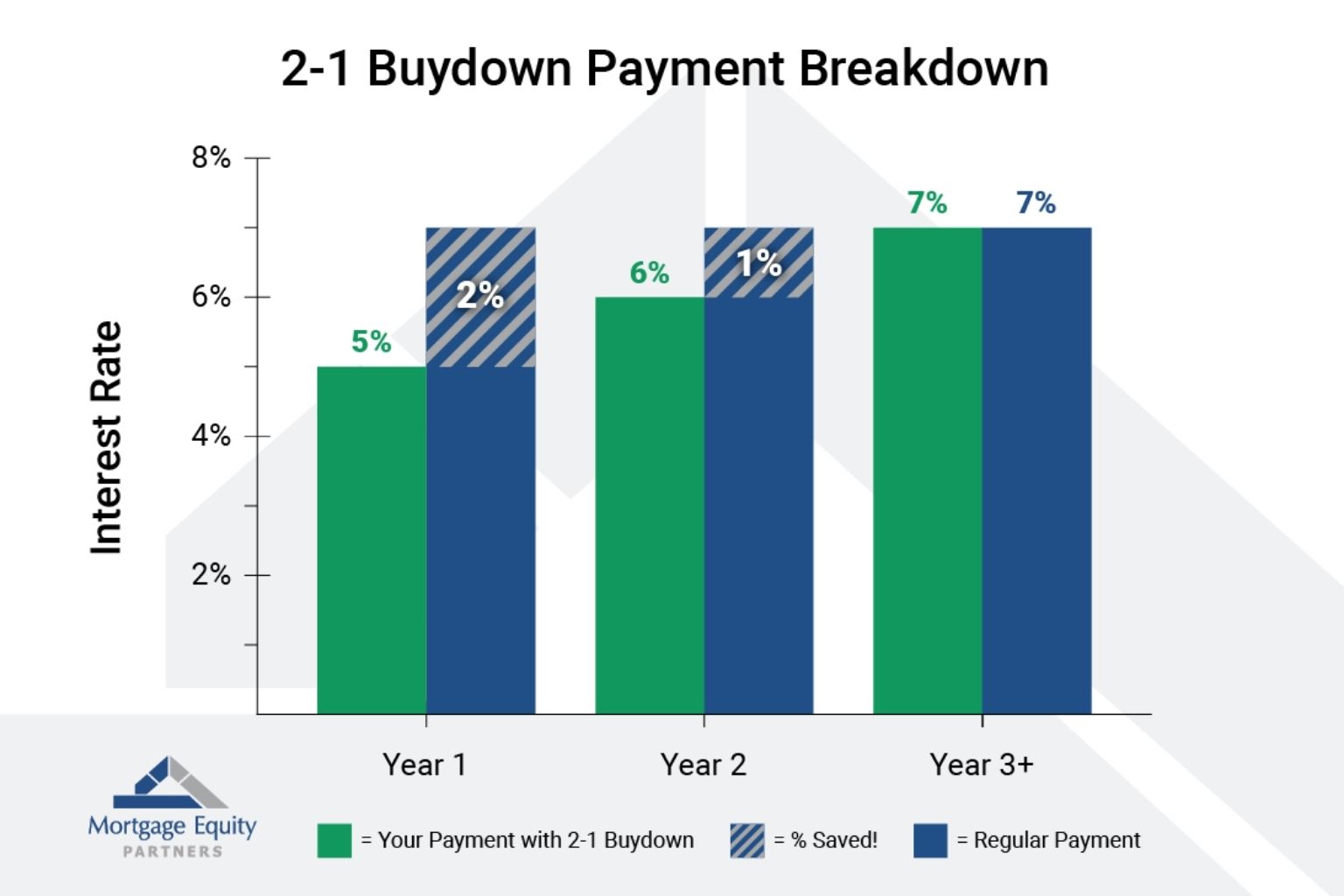

What Buyers Should Know About 2/1 Interest Rate Buydowns

A 2/1 interest rate buydown is a temporary interest rate reduction funded upfront. It’s a powerful tool for buyers when rates are higher today but expected to drop, or when you anticipate income growth in the near future.

Source: mortgageequitypartners.com

How It Works:

- Year 1: Rate is 2% lower than the note rate.

- Year 2: Rate is 1% lower than the note rate.

- Year 3+: Rate returns to the full note rate.

Example: If today’s rate is 6.5%:

- Year 1 payment is based on 4.5%

- Year 2 payment is based on 5.5%

- Year 3+ payment is based on 6.5%

Why It’s Important for Buyers:

- Lower early payments free up cash for furnishing, repairs, or savings.

- Income growth advantage: Many buyers see salary increases, promotions, or business growth within the first two years, making the Year 3 payment more manageable.

- Refinance potential: If rates drop before Year 3, you can refinance — and here’s the key benefit…

What Happens if You Refinance Early?

The difference between the note rate payment and the reduced payment is prepaid interest held in a buydown escrow account.

- If you refinance early (say, after Year 1), the unused prepaid interest is applied directly to your loan principal — reducing your balance.

- This means you don’t “lose” the buydown benefit if you refinance early.

Who Can (and Can’t) Pay for a 2/1 Buydown:

- Must be paid for by the seller (or builder in new construction).

- Cannot be paid for by the buyer.

- Cannot be paid for by the lender.

- This is different from a permanent interest rate buydown (paying points), where a buyer can use their own funds to reduce the rate for the life of the loan.

Pro Tip: Negotiate the buydown as part of your purchase contract’s seller concessions to maximize your early savings.

How Interest Rate Changes Are Handled: Rate Locks & Float-Down Options

Mortgage interest rates in Arizona — and nationwide — can change daily, sometimes multiple times a day. This means the rate you hear from your lender or agent early in the process may not be the rate you close with unless you lock it in.

When Does Your Lender Lock Your Rate?

- A rate lock is not automatic — your lender will only lock in your interest rate when you request it, or when you both agree the timing is right.

- Most buyers lock their rate after going under contract on a home, not before.

- Locks are typically good for 30, 45, or 60 days — your lender will recommend a term that matches your expected closing date.

Why Lock Your Rate?

- Protection from rate increases: Once locked, your interest rate cannot go up, even if market rates rise before closing.

- Gives you certainty in monthly payments, which helps with budgeting.

What Happens if Rates Drop While You’re in Escrow?

- Standard lock: Your rate stays the same, even if rates fall.

- Float-down option: Some lenders offer a float-down provision, allowing you to take advantage of a lower rate if rates drop before closing.

- May come with a small fee.

- Often only available if rates drop by a certain minimum amount (e.g., 0.25% or more).

Questions to Ask Your Lender:

- When will my rate be locked? (Don’t assume it’s automatic.)

- How long will my lock be good for?

- Is there a float-down option if rates drop?

- What happens if my closing is delayed? (Some lenders may charge a fee to extend the lock.)

Pro Tip: Timing matters. Work closely with your lender and real estate agent to choose the optimal time to lock based on your contract timeline and the current rate environment.

Buyer Readiness: How to Keep Your Loan Approval on Track

Once you’re under contract, your lender will need specific documentation and timely cooperation to keep your loan moving smoothly.

Be prepared to:

- Provide two years of W-2s (or 1099s if self-employed).

- Provide two years of federal tax returns.

- Show recent pay stubs and bank statements — and be ready to provide updated versions throughout the loan process if requested.

- Respond to lender requests quickly — delays can jeopardize your closing date.

Avoid these mistakes while under contract:

- Don’t quit or change jobs — lenders will likely verify your employment on the day they fund the loan.

- Don’t make major purchases like furniture, appliances, or a new car — even if financed, these can increase your debt-to-income ratio.

- Avoid large cash withdrawals or spending that depletes your savings — your lender may require proof of cash reserves.

- Don’t open new credit accounts — this can lower your credit score and change your loan approval terms.

Gift Funds for Down Payment or Closing Costs:

- Buyers can receive down payment assistance from family members as a financial “gift.”

- This is common — many parents or grandparents are happy to help loved ones purchase their first home.

- Lenders require a gift letter confirming the money is a gift, not a loan, along with documentation showing the transfer of funds.

- Ask your lender for exact rules and timelines before receiving or depositing gift funds, as the process must be properly documented to avoid approval delays.

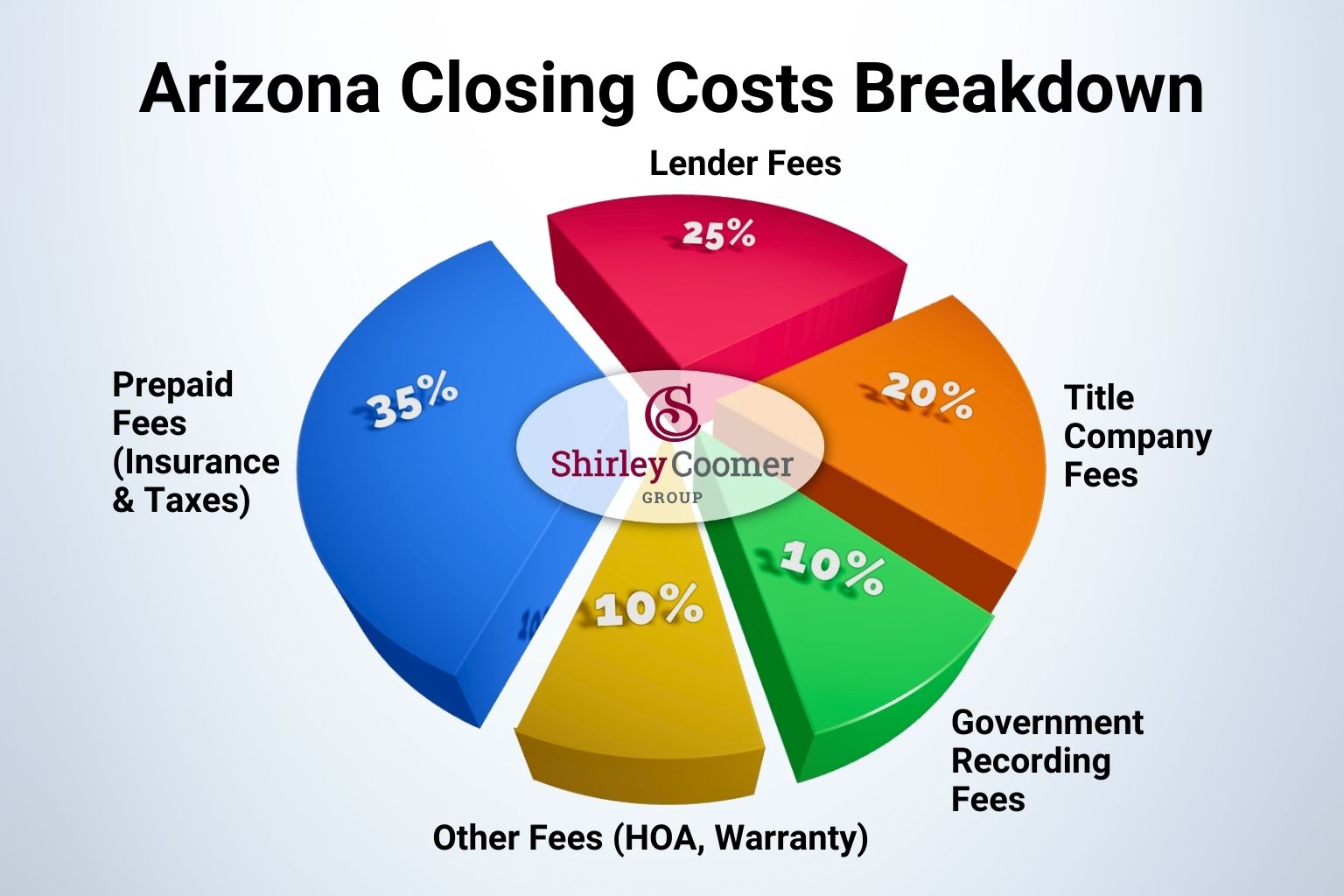

Understanding Closing Costs in Arizona

When buying a home, the purchase price isn’t the only cost to plan for. Closing costs are the fees and prepaid expenses required to finalize your home purchase and get the keys.

While amounts vary depending on your lender, title company, and property location, closing costs in Arizona typically range from 2% to 4% of the purchase price.

Here’s what they often include:

1. Prepaid Expenses (Reserves)

These are upfront payments collected by your lender to ensure certain bills are paid on time.

- One year of homeowner’s insurance (paid in full at closing).

- Reserves for homeowner’s insurance – usually 2–3 months, held in escrow.

- Reserves for property taxes – typically 2–6 months, depending on when taxes are due in your county.

2. Lender Fees

Charged by your lender for processing and funding your loan:

- Loan origination fee

- Underwriting and processing fees

- Credit report fee

- Appraisal fee

- Flood certification fee (if applicable)

3. Title Company Fees

Title companies ensure you receive clear ownership of the property and handle the legal transfer of ownership. Fees include:

- Escrow fee – covers the cost of managing the transaction.

- Title insurance – protects against unknown claims to the property.

- Document preparation fee.

- Courier / wire fees for transferring funds securely.

4. Government Recording Fees

- County recording fee – to officially record the deed and mortgage with the county.

5. Other Possible Costs

- HOA transfer or disclosure fees – if the property is in a community with a Homeowner’s Association.

- Home warranty – sometimes purchased by the buyer for peace of mind.

Lender’s Required Loan Estimate

By law, your lender must provide you with a Loan Estimate within three business days of going under contract. This document includes:

- An estimate of all lender fees.

- Specific title fees (your lender will contact the title company chosen for your transaction to get actual numbers).

- Prepaid taxes and insurance amounts.

- A summary of total estimated cash needed to close.

This early disclosure allows you to review, compare, and ask questions before moving forward.

Who Pays for Closing Costs in Arizona?

Closing costs are part of every real estate transaction, but who pays them can vary depending on your contract negotiations.

Typical Buyer Responsibility:

In most Arizona home purchases, the buyer pays the majority of closing costs. This includes:

- Lender fees (origination, underwriting, appraisal)

- Title company escrow fees

- Prepaid homeowner’s insurance and property tax reserves

- Government recording fees

- Inspection fees

The buyer can bring the funds to closing in the form of a cashier’s check or wire transfer.

Negotiating Seller-Paid Closing Costs

Your real estate agent can negotiate for the seller to contribute toward your closing costs.

- These are called seller concessions or seller credits.

- Seller contributions can often cover all or part of your lender fees, title fees, and even prepaid expenses like insurance and taxes.

- Seller concessions are limited by loan type (FHA, VA, Conventional each have different limits).

Why Seller Concessions Can Be a Win-Win

- For buyers: Reduces the amount of cash you need to bring to closing.

- For sellers: Helps attract more buyers, especially in a slower market.

- In some cases, sellers may agree to concessions instead of lowering the home’s purchase price.

Pro Tip: Even if the seller covers your closing costs, you’ll still need to pay for inspection fees during escrow and your earnest money deposit upfront.

Other Home-Buying Costs to Plan For

In addition to closing costs, buyers should also budget for inspection and due diligence fees. These are typically out-of-pocket expenses paid after going under contract and before closing — and they are not usually refundable.

While these costs can vary depending on the property type and location, here are the most common in Arizona home purchases:

- General Home Inspection – evaluates the property’s overall condition, including structure, plumbing, electrical, and major systems.

- Termite / Wood-Destroying Organism (WDO) Inspection – important in Arizona’s climate where termites are common.

- Roof Inspection – especially valuable for older homes or if the general inspection notes potential roof issues.

- Pool / Spa Inspection – checks pool equipment, plumbing, and safety features.

- Sewer Scope – uses a camera to check for blockages, cracks, or tree root intrusions in sewer lines.

- HVAC (AC & Heating) Inspection – ensures air conditioning and heating units are functioning properly (critical in Arizona summers).

Estimated Range of Inspection Costs in Arizona:

- Home inspection: $350–$600

- Termite inspection: $75–$125

- Roof inspection: $150–$250

- Pool/spa inspection: $75–$150

- Sewer scope: $125–$250

- HVAC inspection: $100–$200

Pro Tip: Even though these inspections are optional, they can uncover costly issues before you’re locked into the purchase. Skipping them to “save” a few hundred dollars could cost you thousands later.

Homeowner’s Insurance: Shop Smart

Your lender will require homeowner’s insurance before closing to protect the property — and their investment. While your lender will include an estimate for insurance in your Loan Estimate, you should shop around to get the best combination of coverage and price.

Smart Insurance Shopping Tips:

- Get quotes from multiple insurance agents — prices can vary significantly.

- Compare policies with different deductibles: $500, $1,000, $5,000.

- Higher deductibles usually mean lower monthly premiums but higher out-of-pocket costs if you file a claim.

- Ask about bundling home and auto insurance for discounts.

- Confirm what the policy covers:

- Replacement cost coverage pays to rebuild or replace items at today’s prices.

- Actual cash value coverage deducts depreciation from the payout.

- Ask if there are discounts for:

- A sprinkler system.

- A monitored security system.

- A newer roof.

Pro Tip: Start shopping for homeowner’s insurance as soon as you go under contract. Waiting until the last minute can lead to higher premiums or rushed decisions — and you’ll want time to compare coverage details, not just prices.

HOA Fees in Arizona Communities

If you’re buying in a community with a Homeowner’s Association (HOA):

- Fees can range from $25–$200+ per month (or higher in some communities).

- They may cover amenities such as pools, fitness centers, tennis courts, landscaping, and common area maintenance.

- Always factor HOA fees into your monthly housing budget.

Pro Tip: Ask your lender how HOA dues may affect your debt-to-income ratio (DTI) since they count toward your monthly housing expenses.

What Buyers Should Look For in a Real Estate Agent

A great real estate agent is more than just someone who schedules showings — they are your guide, advocate, and problem-solver from the first consultation to closing day.

1. Experience With the Lending Process

- Understands different loan programs and how they impact your buying power.

- Can recommend reputable lenders with proven track records.

- Knows how to align contract timelines with your loan approval process.

2. Skilled Negotiator

- Negotiates purchase price based on market data.

- Secures seller concessions for rate buydowns, closing costs, or home warranties.

- Protects you during inspection and appraisal negotiations.

3. Buyer Consultation

- Offers a buyer consultation before you start touring homes.

- Reviews the Arizona purchase contract in detail — even if you’ve bought homes before, laws and forms have likely changed.

- Answers questions about the home-buying process so you know what to expect.

Pro Tip: Even experienced buyers benefit from a consultation. If you’ve purchased in another state or years ago, the Arizona purchase contract has changed over time, and a knowledgeable agent will ensure you understand your rights and obligations before you make an offer.

4. Market Knowledge

- Knows local market trends and neighborhood values.

- Identifies red flags that could affect resale value.

5. Professional Network

- Has trusted inspectors, lenders, insurance agents, and contractors.

- Can connect you with specialists for pools, roofs, HVAC, and more.

6. Communication Skills

- Keeps you informed at every step.

- Explains complex terms in plain language.

7. Problem-Solving Ability

- Anticipates and prevents potential issues.

- Adjusts quickly if an inspection reveals problems or financing needs change.

8. Positive Client Reviews & Success Stories

- Can share examples of past clients who saved money through their negotiation skills.

- Has a track record of closing deals smoothly and on time.

Conclusion

Getting a mortgage in Arizona doesn’t have to be overwhelming. With the right preparation, a knowledgeable lender, and an experienced agent, you can navigate the process confidently — and potentially save thousands in the process.

Whether it’s understanding FHA vs Conventional loans, exploring a 2/1 interest rate buydown, or negotiating seller concessions for closing costs, the more informed you are, the smoother the journey will be.

Your home purchase is one of the biggest financial decisions of your life — and with the right guidance, it can also be one of the most rewarding.

📞 Call or Text: 602-770-0643 📧 Email: scoomer@kw.com

About the Author

Shirley Coomer

602-770-0643

Licensed Realtor® | Keller Williams Realty

Certified Member of the KW Planner Community

Shirley Coomer is a trusted real estate advisor with over two decades of experience helping clients across Arizona protect their wealth and invest strategically. She specializes in 1031 Exchanges, passive income strategies, and wealth planning for investors and retirees.